(0) Retail sales on a headline level came in close to consensus, with a +0.1% gain for January. When sales ex-automobiles were removed, the growth bumped to +0.2%, which was a tenth of a percent better than expected. Lastly, the ‘core/control’ number (which attempts to normalize things by excluding cyclical autos, gasoline stations and building materials—per what the government uses in their GDP calculations) rose +0.1% for the month, which was lower than the forecast +0.3%. In the core figure, ‘misc.’ retailers such as office supply were down over two percent, while department stores were stronger by roughly a percentage point. Net-net, despite payroll tax hike effects, it appears this year has begun decently in the retail sales arena, albeit with relatively flat numbers.

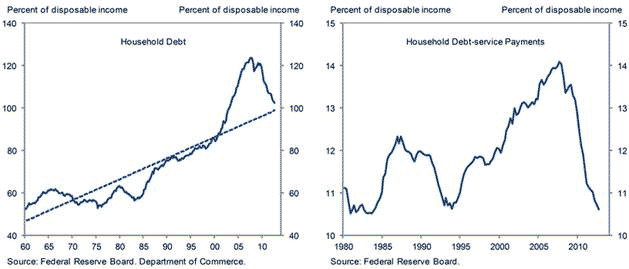

Speaking of the consumer, underlying conditions here have improved as well on several fronts, although we don’t hear much about that. Real wage and salary income growth has picked up to roughly 3% on a year-over-year basis. Secondly, household leverage has been significantly reduced from its peak in the third quarter of 2007 (per the charts shown below), back towards the multi-decade trend. So, one positive from financial crisis was a significant disposal of personal debt. Combining these factors, gets us to a higher level of household net worth, which is back up to roughly 550% of disposable income (from a high of 650% in 2007 and low of 475% or so in 2009). While choppy quarter to quarter, consumer conditions as a whole appear to have improved.

(0) January industrial production fell -0.1%, compared to an expected +0.2%. Core manufacturing, notably in automobiles and car parts. This counteracted gains in utilities production due to colder weather in certain parts of the country. The fourth quarter figure was revised upward to an annualized rate of +1.9% from +0.2% as well. Capacity utilization, on the other hand, finished the month at 79.1% versus a consensus number of 78.9%.

(+) The Univ. of Michigan consumer sentiment survey rose to 76.3, which was higher than the expected 74.8 level. Assessments for both current conditions and future prospects were higher—roughly at the same magnitude. Interestingly, households with incomes below $75k were the primary driver of the higher sentiment.

(0) Business inventories rose +0.1%, which was a tenth of a percent below expected. However, the figure was larger than the government included in its first GDP estimate for the fourth quarter, so this may improve the second revision.

(+) The New York Empire manufacturing survey posted a +17.8 gain for February, bring the index to +10—much stronger than the expected -2 reading. Underlying metrics were also good, with new orders, shipments and employment all higher. Expectations for forward-looking capital activity were also much stronger. This only one state so this has to be taken in context, but it is a large one, and we’ll take it.

(+) Initial jobless claims for the Feb. 9 ending week fell to 341k, which was an improvement compared to the expected 360k result. There remain some seasonal adjustment issues in the weekly data, but the four-week moving average has remained roughly in the 350k range. Continuing claims for the Feb. 2 week came in at 3,114k, which was a bit lower than the 3,205k expected and proceeded along a trend of post-crisis lows. These numbers are choppy for sure, but have steadily looked better on an average level as the months have progressed.

(0) The NFIB small business optimism index rose 0.9 of a point to 88.9 for January, which was just a few tenths below the anticipated figure. Despite improvement, the figure remains in the ‘depressed’ category after a huge November 2012 drop during the high point of fiscal cliff uncertainty. The percentage of survey respondents that expect the economy to improve rose a bit, but remains at only about 30%. At the same time, though, these respondents were much more optimistic about conditions in their own businesses.

Small business owners, as has the general public, have been quite pessimistic about headwinds they believe government has created through political wranglings, a heightened environment of regulation (in the Obama administration in particular) and uncertainty in the tax code. This naturally manifests itself in several ways, including hesitation to make shorter-term capital investments and hire additional workers—even if they’re needed. Improved figures here are a start, but may continue to be sporadic as overall economic growth remains slow and political issues continue to fester.

From a larger business perspective, optimism also improved, as noted by the Morgan Stanley Business Conditions Index for February. The bulk of this improvement was due to expectations a few quarters down the road that government policy hurdles/risks will eventually fade into the background. The employment situation continues to look a bit weak, however—perpetuating the woes in labor pick-up the Fed has lamented over in their communications. Conditions appear most improved in consumer goods and technology (with better growth prospects).

Market Notes

|

Period ending 2/15/2013 |

1 Week (%) |

YTD (%) |

| DJIA |

0.08 |

7.11 |

| S&P 500 |

0.20 |

6.86 |

| Russell 2000 |

1.07 |

8.80 |

| MSCI-EAFE |

-0.49 |

3.86 |

| MSCI-EM |

0.53 |

1.07 |

| BarCap U.S. Aggregate |

-0.04 |

-0.65 |

| U.S. Treasury Yields |

3 Mo. |

2 Yr. |

5 Yr. |

10 Yr. |

30 Yr. |

| 12/31/2012 |

0.05 |

0.25 |

0.72 |

1.78 |

2.95 |

| 2/8/2013 |

0.07 |

0.25 |

0.84 |

1.99 |

3.17 |

| 2/15/2013 |

0.10 |

0.29 |

0.87 |

2.01 |

3.18 |

Stocks experienced a flat week for the most part, with highlights coming from small caps, which have quietly become the year-to-date leaders from a market cap perspective. In the S&P, industrials and financials outperformed, while telecom service and technology lagged.

Internationally, emerging market stocks outearned developed market equities overall, but the country-by-country results were fairly mixed. South Korea, China, Australia and Brazil all ended up higher, while Japan, India, Italy and Mexico were among the worst performing indexes for the week. From an economic perspective, Eurozone GDP came in at -2.3% annualized for the fourth quarter, confirming continued weakness (France was best at -0.3%, but still negative, nonetheless).

The Treasury yield curve flattened as interest rates on the short end rose, while longer-term rates were strangely little changed from the previous week. The best performing bond assets were U.S. high yield and floating rate bank loan, which have continued to see strong cash flows in recent weeks. Most investment grade debt lost a few basis points, led by TIPs, and emerging market bonds, which fared the worst—losing roughly 0.50%.

In real estate, mortgage and residential REITs gained well over a percent and a half on the week, while European REITs were also competitive. Asian REITs and U.S. industrial generally lost ground as the worst performing groups.

For the week in commodities, petroleum and industrial metals gained a few tenths of a percent, while grains and precious metals lost ground. Similarly, commodity markets in 2013 have been led by energy—for several reasons, including better sentiment regarding global economic recovery (including emerging market demand growth), and unrest in the Middle East/North Africa region. Gasoline prices have seen strength in addition to this due to lower supply conditions from refinery downtime activity in anticipation of summer. Along the same lines as the better environment for energy prices overall (global growth), precious metals returns have disappointed due to the crisis concerns that gold relies on for price appreciation have dissipated somewhat. This is also related to less negative real bond yields and lower implied risk levels for equities as of late.

Have a good week.

Karl Schroeder, RFC

Investment Advisor Representative

Schroeder Financial Services, Inc.,

Sun Lakes, AZ

Sources: FocusPoint Solutions, Associated Press, Barclays Capital, Bloomberg, Deutsche Bank, FactSet, Goldman Sachs, JPMorgan Asset Management, Morgan Stanley, MSCI, Morningstar, Northern Trust, Oppenheimer Funds, Payden & Rygel, PIMCO, Thomson Reuters, Schroder’s, Standard & Poor’s, U.S. Bureau of Economic Analysis, U.S. Federal Reserve, Wells Capital Management, Yahoo!, Zacks Investment Research. Index performance is shown as total return, which includes dividends, with the exception of MSCI-EM, which is quoted as price return/excluding dividends. Performance for the MSCI-EAFE and MSCI-EM indexes is quoted in U.S. Dollar investor terms.

The information above has been obtained from sources considered reliable, but no representation is made as to its completeness, accuracy or timeliness. All information and opinions expressed are subject to change without notice. Information provided in this report is not intended to be, and should not be construed as, investment, legal or tax advice; and does not constitute an offer, or a solicitation of any offer, to buy or sell any security, investment or other product. Schroeder Financial Services, Inc. is a registered investment advisor.

Notes key: (+) positive/encouraging development, (0) neutral/inconclusive/no net effect, (-) negative/discouraging development.